Why South Korean family offices are joining the rush to Singapore

Each of Asia’s leading family office hubs are gateways to economically important regions. Hong Kong connects the world to mainland China, and vice versa. Dubai is a major access point for the Middle East and Africa. But one of the fastest growing destinations for managing family wealth is Singapore, thanks to both favorable policies and its geographical position as a springboard to opportunities in the dynamic Association of Southeast Asian Nations (ASEAN) region. That’s luring firms from around Asia – and notably from South Korea – to setup shop in the Southeast Asian city-state.

By the end of 2023, 1,400 single-family offices (SFOs) had been established in Singapore,[1] many taking advantage of the Variable Capital Company (VCC) structure introduced there in 2020. Although it has robust requirements, the VCC structure offers several key advantages, including tax-exempt distributions of dividends to shareholders[2] and privacy protections – the register of members of a VCC does not need to be disclosed publicly.[3]

The VCC structure embraced by family offices is just one example of the pro-investment policy stance that has helped make tiny Singapore, spanning just over 700 sq. km and home to nearly 6 million people, one of the preferred destinations for millionaire migrants globally. It is forecast to receive the world’s third largest net inflow of high-net-worth individuals in 2024, following closely behind the United Arab Emirates in the top spot and the US in No. 2.[4]

The city-state presents an attractive living environment for the well-heeled. The leafy, equatorial city is safe, clean, well-run, and boasts excellent schools and healthcare. And in contrast to the worsening political polarization spreading in many countries, Singapore stands out for its stability.

Oasis of calm

Of the 29 countries covered in a recent Ipsos poll on key social and political issues, Singapore came out on top, with 79% of citizens stating they believed their country is heading in the right direction, compared with a global average of only 38%.[5]

In May 2024, Singapore’s former Prime Minister Lee Hsien Loong passed the baton to his party’s chosen successor, Lawrence Wong, in an orderly transition that throws into sharp relief the sense of trepidation around other major elections later this year, most notably the contest in the US.[6]

According to consultancy EY, geopolitics has displaced inflation in 2024 as the No. 1 issue affecting the investment decisions of family offices.[7] This is also expected to drive more wealthy families to relocate their investment office operations to destinations like Singapore.

This shift is happening against the backdrop of a momentous transfer of inter-generational wealth, which has spurred a rise of single-family offices across the globe.[8] As Asia’s richest families prepare to hand down US$2.5 trillion in wealth by 2030, Singapore family offices look set to feature more prominently in succession plans.[9]

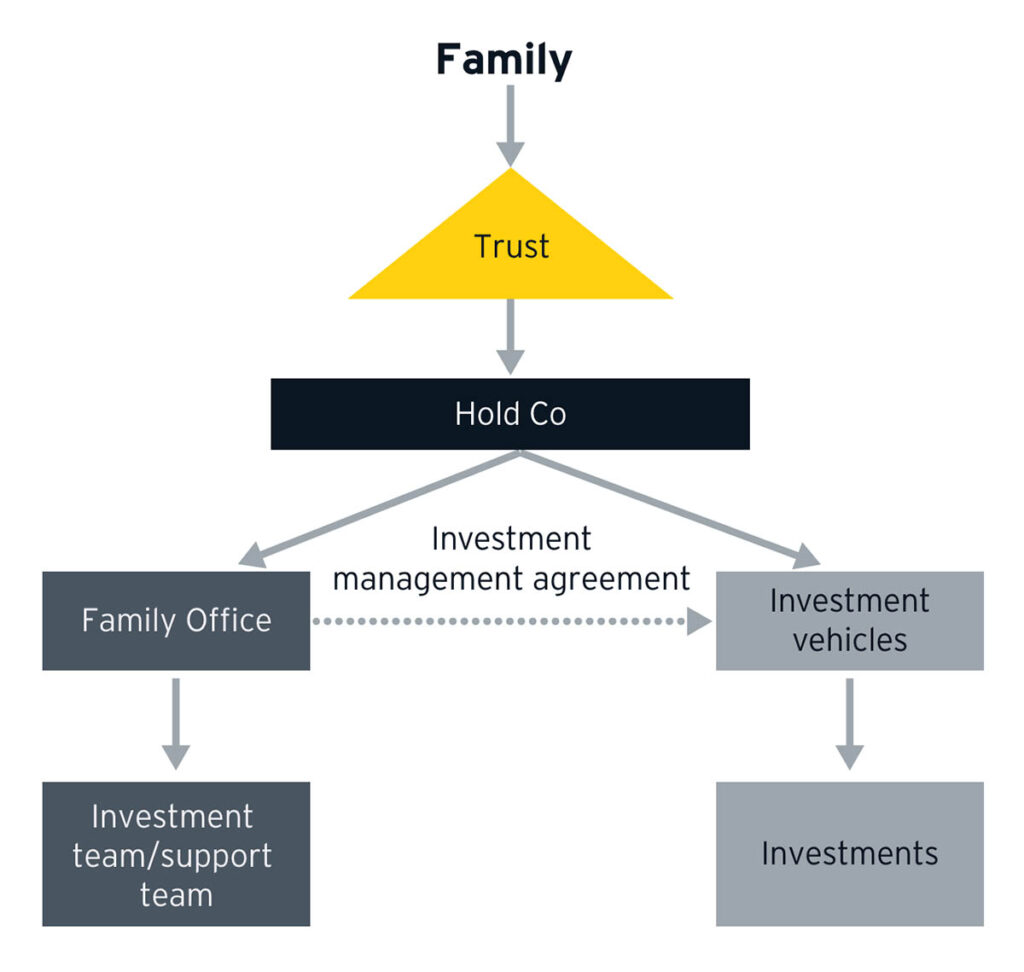

To this end, many families across Asia are looking to restructure the ownership of their businesses from legacy structures to holding structures domiciled in Singapore using the VCC fund structure, with a case-in-point being South Korea. Increasingly, South Korean family offices are looking to leverage the VCC structure in Singapore to access a wide range of opportunities globally, or around ASEAN, or even back at home. For instance, AIP Investment Partners, part of the Seoul-headquartered AIP group of asset management companies, uses the VCC platform in Singapore to invest alongside family offices in Korean startups in the growth stage.[10]

The rise of South Korean family offices moving to Singapore is a reflection of the increasing focus of the country’s businesses on ASEAN. Ties between South Korea and ASEAN have deepened steadily since they signed a deal for a free trade agreement in 2005.[11]

Today, ASEAN is the most popular destination for Korean travelers, and Korea’s second largest trading partner and investment destination.[12] What’s more, the relationship is set to become even closer as South Korea’s corporates look to ASEAN as a manufacturing base to diversify their supply chains.[13]

Seeking wealth preservation

Recent events at home may also have bolstered Singapore’s appeal to wealthy Koreans. Hopes that South Korea might cut its inheritance tax rates — among the highest in the developed world — were dashed following the country’s legislative election in April 2024.[14] The party of President Yoon Suk Yeol, who had been looking to reduce the levy, suffered a landslide defeat. The newly emboldened opposition bloc in parliament wants the wealthy to pay more taxes.

Heirs of chaebol, Korea’s large family-controlled conglomerates, may be subject to hefty taxes on shares they inherit. After Samsung patriarch Lee Kun-hee’s death in 2020, for example, his heirs had to sell approximately USD2 billion worth of company shares to pay off inheritance taxes due.[15]

The high inheritance tax rate may be one factor prompting more wealthy Koreans to emigrate and move their assets offshore. South Korea lost the world’s seventh-highest number of wealthy people to emigration in 2023.[16]

For the investment community, the planned introduction of a capital-gains tax in 2025 is another cause for concern — in fact, South Korea’s top financial watchdog has warned that if it goes ahead, retail investors might sour on the local stock market.[17]

Singapore, by contrast, has no inheritance tax or capital gains tax on the sale of financial instruments,[18] and low personal and corporate income taxes. And given its political stability, and its generally pro-investment policy stance, this tax regime appears unlikely to face radical changes in the near term. That’s yet one more reason why Singapore’s appeal as a family office hub is likely to grow.

For families with concentrated shareholdings wishing to diversify their portfolios, equities-backed financing from EquitiesFirst provides a convenient, cost-effective means of raising capital to fund investments through any one of the world’s wealth management hubs - including Singapore.

Past performance does not guarantee future returns, and individual returns are not guaranteed or warranted.

This Document is intended solely for accredited investors, sophisticated investors, professional investors, or otherwise qualified investors, as may be required by law or otherwise, and it is not intended for, and should not be used by, persons who do not meet the relevant requirements. The content provided herein is for informational purposes only and is general in nature and not targeted to any specific objective or financial need. The views and opinions expressed in this Document have been prepared by third parties and do not necessarily reflect the views and opinions of EquitiesFirst. EquitiesFirst has not independently examined or verified the information provided herein, and no representation is made that it is accurate or complete. Opinions and information herein are subject to change without notice. The content provided does not constitute an offer to sell (or solicitation of an offer to purchase) any securities, investments, or any financial products (“Offer”). Any such Offer shall only be made through a relevant offering or other documentation which sets forth its material terms and conditions. Nothing contained in this Document shall constitute a recommendation, solicitation, invitation, inducement, promotion, or offer for the purchase or sale of any investment product by Equities First Holdings, LLC or its subsidiaries (collectively, “EquitiesFirst”), nor shall this Document be construed in any way as investment, legal, or tax advice, or as a recommendation, reference, or endorsement by EquitiesFirst. You should seek independent financial advice prior to making an investment decision about a financial product.

This Document contains the intellectual property of EquitiesFirst in the United States and other countries, including, without limitation, their respective logos and other registered and unregistered trademarks and service marks. EquitiesFirst reserves all rights in and to their intellectual property contained in this Document. The Document should not be distributed, published, reproduced or otherwise made available in whole or in part by recipients to any other person and, in particular, should not be distributed to persons in any country where such distribution may lead to a breach of any legal or regulatory requirement.

EquitiesFirst make no representation or warranty with respect to this Document and expressly disclaim any implied warranty under law. You acknowledge that EquitiesFirst is not liable under any circumstances for any direct, indirect, special, consequential, incidental, or punitive damages whatsoever, including, without limitation, any lost profits or lost opportunity, even if EquitiesFirst has been advised of the possibility of such damages.

EquitiesFirst makes the following further statements that may be applicable in the stated jurisdiction:

Australia: Equities First Holdings (Australia) Pty Ltd (ACN: 142 644 399) holds an Australian Financial Services Licence (AFSL Number: 387079). All rights reserved.

The information contained on this Document is intended for persons located in Australia only and classified as a Wholesale Client only as defined in Section 761G of the Corporations Act 2001. The distribution of information to persons outside this criteria may be restricted by law and persons who come into possession of it should seek advice and observe any such restriction.

The material contained in this Document is for information purposes only and should not be construed as an offer or solicitation or recommendation to buy or sell financial products.

The information contained in this Document is intended to be general in nature and is not personal financial product advice. Any advice contained in the Document is general advice only and has been prepared without considering your objectives, financial situation or needs. Before acting on any information, you should consider the appropriateness of the information provided and the nature of the relevant financial product having regard to your objectives, financial situation and needs. You should seek independent financial advice and read the relevant disclosure statements or other offer documents prior to making an investment decision about a financial product.

Forecasts are not guaranteed, and undue reliance should not be placed on them. This information is based on views held by Equities First Holdings (Australia) Pty Ltd as at the publishing date of this material.

Dubai: Equities First Holdings Hong Kong Ltd (DIFC Representative Office) at Gate Precinct Building 4, 6th Floor, Office 7, Dubai International Financial Centre (commercial license number CL7354) is regulated by the Dubai Financial Services Authority (“DFSA”) as a Representative Office (DFSA Firm Reference No.: F008752). All rights reserved.

The information contained in this document is intended to be general in nature, and, to the extent that it is perceived as advice, any advice contained in this document is general advice only and has been prepared without considering your objectives, financial situation, suitability of the financial products or your needs.

The material contained in this document is for information purposes only and should not be construed as financial advice, including an offer or solicitation or recommendation to buy or sell financial products. The information contained in this document is intended to be general in nature and any advice contained in this document is general advice only and has been prepared without considering your objectives, financial situation, suitability of the financial products or your needs. Before acting on any information, you should consider the appropriateness of the information provided and the nature of the relevant financial product having regard to your objectives, financial situation and needs. If you do not understand the contents of this document, you should consult an authorised financial adviser.

This document relates to a financial product which is not subject to any form of regulation or approval by the DFSA. The DFSA has no responsibility for reviewing or verifying any documents in connection with this financial product. Accordingly, the DFSA has not approved this document or any other associated documents nor taken any steps to verify the information set out in this document, and has no responsibility for it.

Hong Kong: Equities First Holdings Hong Kong Limited is licensed under the Money Lenders Ordinance (Money Lender’s Licence No. 1659/2024) and to carry on the business of dealing in securities (Type 1 licence) under the Securities and Futures Ordinance (“SFO”) (CE No. BFJ407). This Document has not been reviewed by the Hong Kong Securities and Futures Commission. It is not intended as an offer to sell securities or a solicitation to buy any product managed or provided by Equities First Holdings Hong Kong Limited and is only intended for persons who qualify as Professional Investors under the SFO. This document is not directed to individuals or organizations for whom such offers or invitations would be unlawful or prohibited.

Korea: The foregoing is intended solely for sophisticated investors, professional investors or otherwise qualified investors who have sufficient knowledge and experience in entering into securities financing transactions. It is not intended for, and should not be used by, persons who do not meet those criteria.

United Kingdom: Equities First (London) Limited is authorised and regulated in the UK by the Financial Conduct Authority (“FCA”). In the UK, this Document is only being distributed and made available to persons of the kind described in Article 19(5) (investment professionals) and Article 49(2) (high net worth companies, unincorporated associations etc.) of Part IV of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (‘’FPO’’) and any investment activity to which this presentation relates is only available to, and will only be engaged in with, such persons. Persons who do not have professional experience in matters relating to investment or who are not persons to whom Article 49 of the FPO applies should not rely on this document. This Document is only prepared for and available to persons who qualify as Professional Investors under the Markets in Financial Instruments Directive.