IPO Exit Opportunities are Dawning for the Middle East’s Burgeoning Fintech Sector

25 July 2024 Every technology startup investor should have an exit strategy. One of the most desirable can be an initial public offering (IPO). When a startup goes public, its founders and early investors have the option of either cashing out entirely, or remaining invested as the company uses its IPO proceeds to further grow and expand.

Until recently, the lack of dynamism in the Middle East IPO market was seen as an impediment to the region’s hopes of establishing a vibrant technology ecosystem.[1] Now, even as listing activity elsewhere in the world flounders, the region is witnessing an IPO boom[2] that’s paving the way for IPO exits. This should add further fuel to the expansion of the Middle East’s flourishing technology sector.

Underserved Opportunity

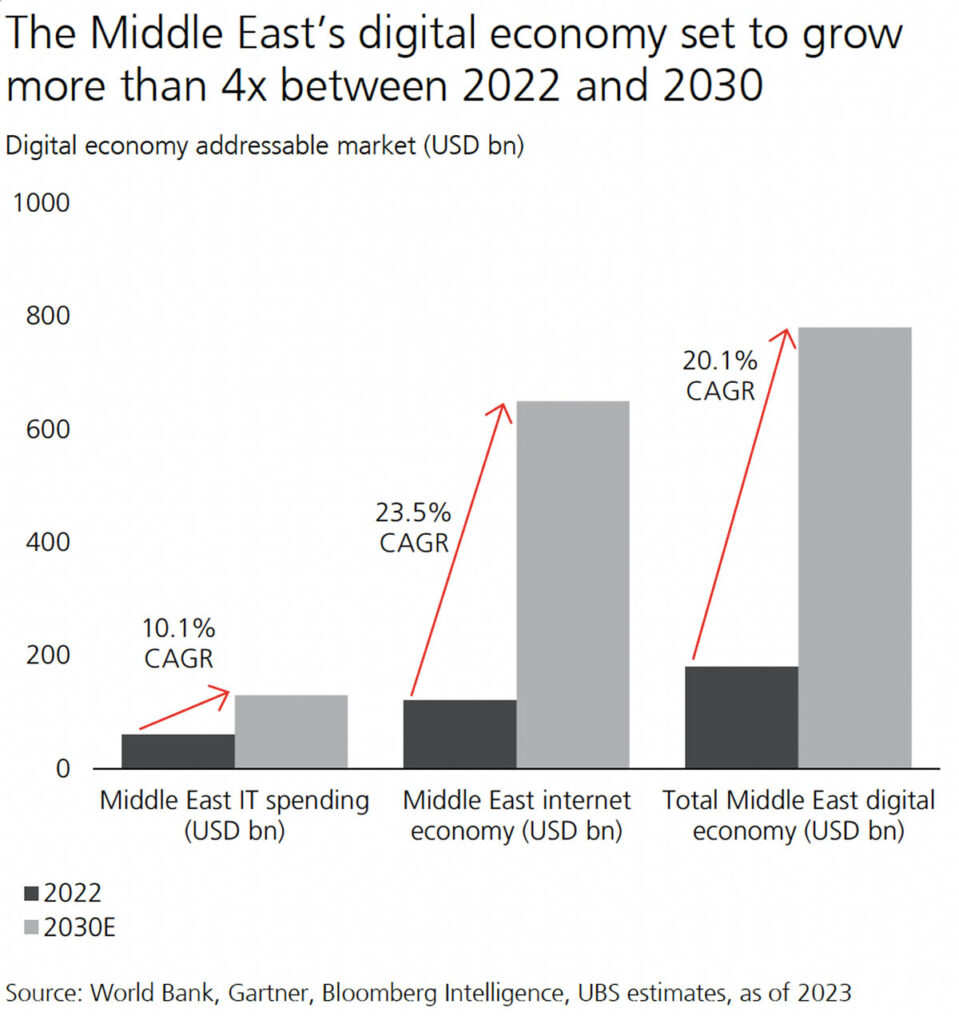

Tech entrepreneurs are being drawn to the sheer size of the opportunity in the region. The growth of the Middle East’s digital economy is expected to outstrip that of the rest of the world by a fair margin in the coming years, according to the TechGPT Compendium published by Swiss investment bank UBS.[3]

The region’s digital economy is still relatively underpenetrated, worth about USD180 billion, or 4.1% of GDP, compared to penetration rates of 10.5% globally, 15% in the US, and 7.4% in India. But the stage is set for the Middle East to rapidly close that gap. Between now and 2030, its digital economy is tipped by UBS to grow at 20% per annum – double the global rate – reaching $780 billion, or 13.4% of GDP, by the end of the current decade (see Figure 1).[4]

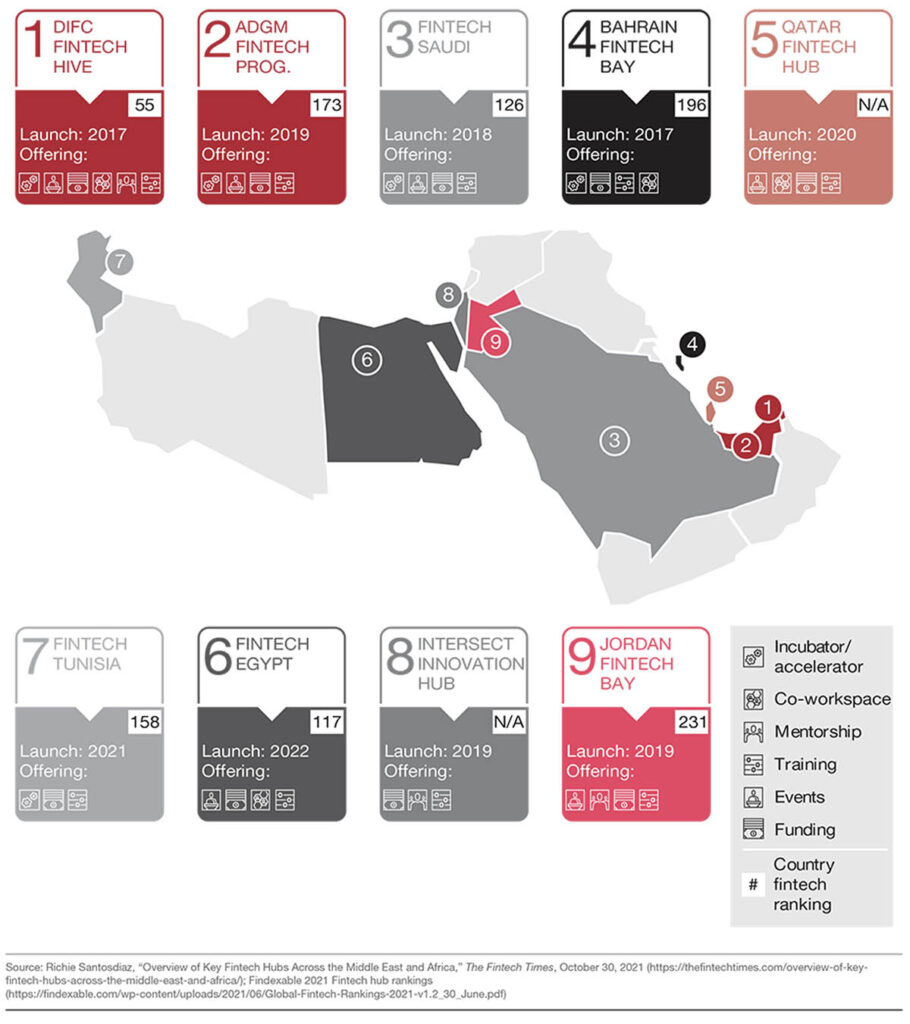

Among the various tech segments, fintech is leading the charge in the Middle East, with several fintech hubs having emerged across the region to support and channel funding to a host of dynamic startups.

Nine fintech hubs have appeared across the Middle East and North Africa (see Figure 2), led by the FinTech Hive at the Dubai International Financial Centre (DIFC), which opened its doors in 2017. Other globally renowned hubs located in Gulf Cooperation Council (GCC) member nations include the Abu Dhabi Global Market (ADGM); the Bahrain Fintech Bay; the Qatar Fintech Hub; and Fintech Saudi.

Figure 2: Fintech Hubs in the Middle East and North Africa

Fintech attracted $1.4 billion of venture funding in the MENA region in 2023. Since 2021, there have been twice as many deals in fintech as in e-commerce, the second most popular technology segment.[5] The regional fintech segment’s revenues are expected to triple between 2022 and 2025, when they could reach as much as $4.5 billion, according to consultancy McKinsey.[6]

Within fintech, the focus is very much on digital payments, adoption of which was accelerated by the Covid-19 pandemic: in the UAE, for example, non-cash payments rose from 39% in 2018 to 73% in 2023.[7] Government initiatives are also helping, such as Saudi’s Arabia’s Vision 2030 policy, targeting 70% cashless payments by 2025 and the UAE’s efforts to link regional payment systems.[8]

While cash is still king across much of the Middle East, consumer surveys show a strong appetite for digital wallets and contactless payments.[9] Unsurprisingly, payment companies dominate Forbes’ Middle East Fintech 50 list,[10] which ranks the top players revolutionizing the financial technology landscape in the underserved region.

The second biggest category is digital banking, which is also considerably underpenetrated in the region. Only 17% of consumers in the Middle East use digital banking, compared to almost 60% in the US.[11]

Topping Forbes’ Middle East Fintech 50 list is UAE-base Wio Bank, which launched its first digital banking application in 2022. Coming in second is Egypt’s Fawry, a provider of e-payments and digital finance solutions catering to over 52.7 million customers.

For fintechs looking to expand in the region, the UAE is emerging as a preferred base thanks to its supportive regulatory regime, low taxes, well-developed infrastructure, availability of talent (see Figure 2), quality of life, and ability to serve as a gateway to the rest of the region.

Such are the UAE’s attractions that some startup founders boast of being able to lure tech workers from California to relocate there at slightly lower pre-tax salaries.[12] There has been an influx of fintech developers from various parts of the world moving to Dubai and Abu Dhabi,[13] including at cryptocurrency firms attracted by the UAE’s forward-thinking stance on digital assets and tech-savvy local consumer base.[14]

Coming in with a clearer exit

Meanwhile, the IPO frenzy in the Gulf region shows no signs of abating. During 2022/23, Middle Eastern stock markets welcomed 99 IPOs, raising roughly $33 billion combined, according to data from EY.[15]

Although there have been few tech listings so far, that could be set to change following the IPO of Saudi fintech firm Rasan Information Technology in May 2024.[16] Rasan, which provides fintech and insurtech services, started operations in 2017 and serves more than 7.5 million customers in Saudi Arabia.

The IPO boom in Dubai, too, has ample scope to expand.[17] With strong momentum established by privatization of state-related entities and listings by family-owned companies, the next phase of the IPO boom is likely to feature fintechs and other tech firms. By demonstrating lucrative exit options for ambitious entrepreneurs, this could turbocharge the region’s burgeoning startup ecosystem.

Still, with venture investment standing at a five-year low, fintechs and tech entrepreneurs eyeing expansion in the Middle East could find it difficult to access funding in the near term, ahead of global interest rate cuts.[18] Specialty financing could therefore play a vital role in sustaining the Middle East’s fintech momentum and enabling startups to achieve their growth potential in this underserved region.

At this critical juncture in the development of the Middle East’s digital economy, EquitiesFirst has seen strong interest from entrepreneurs seeking to unlock capital from their long-term shareholdings to pursue opportunities across the region.

Past performance does not guarantee future returns, and individual returns are not guaranteed or warranted.

This Document is intended solely for accredited investors, sophisticated investors, professional investors, or otherwise qualified investors, as may be required by law or otherwise, and it is not intended for, and should not be used by, persons who do not meet the relevant requirements. The content provided herein is for informational purposes only and is general in nature and not targeted to any specific objective or financial need. The views and opinions expressed in this Document have been prepared by third parties and do not necessarily reflect the views and opinions of EquitiesFirst. EquitiesFirst has not independently examined or verified the information provided herein, and no representation is made that it is accurate or complete. Opinions and information herein are subject to change without notice. The content provided does not constitute an offer to sell (or solicitation of an offer to purchase) any securities, investments, or any financial products (“Offer”). Any such Offer shall only be made through a relevant offering or other documentation which sets forth its material terms and conditions. Nothing contained in this Document shall constitute a recommendation, solicitation, invitation, inducement, promotion, or offer for the purchase or sale of any investment product by Equities First Holdings, LLC or its subsidiaries (collectively, “EquitiesFirst”), nor shall this Document be construed in any way as investment, legal, or tax advice, or as a recommendation, reference, or endorsement by EquitiesFirst. You should seek independent financial advice prior to making an investment decision about a financial product.

This Document contains the intellectual property of EquitiesFirst in the United States and other countries, including, without limitation, their respective logos and other registered and unregistered trademarks and service marks. EquitiesFirst reserves all rights in and to their intellectual property contained in this Document. The Document should not be distributed, published, reproduced or otherwise made available in whole or in part by recipients to any other person and, in particular, should not be distributed to persons in any country where such distribution may lead to a breach of any legal or regulatory requirement.

EquitiesFirst make no representation or warranty with respect to this Document and expressly disclaim any implied warranty under law. You acknowledge that EquitiesFirst is not liable under any circumstances for any direct, indirect, special, consequential, incidental, or punitive damages whatsoever, including, without limitation, any lost profits or lost opportunity, even if EquitiesFirst has been advised of the possibility of such damages.

EquitiesFirst makes the following further statements that may be applicable in the stated jurisdiction:

Australia: Equities First Holdings (Australia) Pty Ltd (ACN: 142 644 399) holds an Australian Financial Services Licence (AFSL Number: 387079). All rights reserved.

The information contained on this Document is intended for persons located in Australia only and classified as a Wholesale Client only as defined in Section 761G of the Corporations Act 2001. The distribution of information to persons outside this criteria may be restricted by law and persons who come into possession of it should seek advice and observe any such restriction.

The material contained in this Document is for information purposes only and should not be construed as an offer or solicitation or recommendation to buy or sell financial products.

The information contained in this Document is intended to be general in nature and is not personal financial product advice. Any advice contained in the Document is general advice only and has been prepared without considering your objectives, financial situation or needs. Before acting on any information, you should consider the appropriateness of the information provided and the nature of the relevant financial product having regard to your objectives, financial situation and needs. You should seek independent financial advice and read the relevant disclosure statements or other offer documents prior to making an investment decision about a financial product.

Forecasts are not guaranteed, and undue reliance should not be placed on them. This information is based on views held by Equities First Holdings (Australia) Pty Ltd as at the publishing date of this material.

Dubai: Equities First Holdings Hong Kong Ltd (DIFC Representative Office) at Gate Precinct Building 4, 6th Floor, Office 7, Dubai International Financial Centre (commercial license number CL7354) is regulated by the Dubai Financial Services Authority (“DFSA”) as a Representative Office (DFSA Firm Reference No.: F008752). All rights reserved.

The information contained in this document is intended to be general in nature, and, to the extent that it is perceived as advice, any advice contained in this document is general advice only and has been prepared without considering your objectives, financial situation, suitability of the financial products or your needs.

The material contained in this document is for information purposes only and should not be construed as financial advice, including an offer or solicitation or recommendation to buy or sell financial products. The information contained in this document is intended to be general in nature and any advice contained in this document is general advice only and has been prepared without considering your objectives, financial situation, suitability of the financial products or your needs. Before acting on any information, you should consider the appropriateness of the information provided and the nature of the relevant financial product having regard to your objectives, financial situation and needs. If you do not understand the contents of this document, you should consult an authorised financial adviser.

This document relates to a financial product which is not subject to any form of regulation or approval by the DFSA. The DFSA has no responsibility for reviewing or verifying any documents in connection with this financial product. Accordingly, the DFSA has not approved this document or any other associated documents nor taken any steps to verify the information set out in this document, and has no responsibility for it.

Hong Kong: Equities First Holdings Hong Kong Limited is licensed under the Money Lenders Ordinance (Money Lender’s Licence No. 1659/2024) and to carry on the business of dealing in securities (Type 1 licence) under the Securities and Futures Ordinance (“SFO”) (CE No. BFJ407). This Document has not been reviewed by the Hong Kong Securities and Futures Commission. It is not intended as an offer to sell securities or a solicitation to buy any product managed or provided by Equities First Holdings Hong Kong Limited and is only intended for persons who qualify as Professional Investors under the SFO. This document is not directed to individuals or organizations for whom such offers or invitations would be unlawful or prohibited.

Korea: The foregoing is intended solely for sophisticated investors, professional investors or otherwise qualified investors who have sufficient knowledge and experience in entering into securities financing transactions. It is not intended for, and should not be used by, persons who do not meet those criteria.

United Kingdom: Equities First (London) Limited is authorised and regulated in the UK by the Financial Conduct Authority (“FCA”). In the UK, this Document is only being distributed and made available to persons of the kind described in Article 19(5) (investment professionals) and Article 49(2) (high net worth companies, unincorporated associations etc.) of Part IV of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (‘’FPO’’) and any investment activity to which this presentation relates is only available to, and will only be engaged in with, such persons. Persons who do not have professional experience in matters relating to investment or who are not persons to whom Article 49 of the FPO applies should not rely on this document. This Document is only prepared for and available to persons who qualify as Professional Investors under the Markets in Financial Instruments Directive.